Introduction to the 50/30/20 Rule

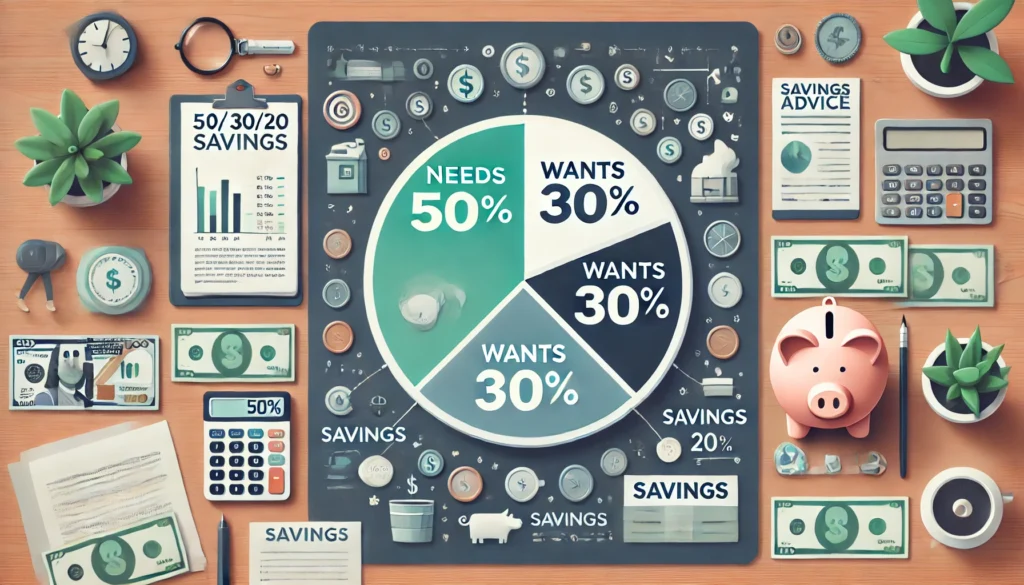

The 50/30/20 savings strategy is a straightforward yet effective budgeting method that has gained traction in personal finance discussions. This rule is built on three fundamental categories: 50% of one’s income is designated for needs—essential expenses such as housing, food, and transportation; 30% is allocated for wants—discretionary expenses that enhance one’s quality of life; and the remaining 20% is earmarked for savings or debt repayment. This method not only simplifies budgeting but also provides a clear framework that individuals can easily adapt regardless of their income levels.

In today’s financial climate, where economic uncertainties and fluctuating costs are prevalent, the 50/30/20 strategy offers a guiding principle for effective money management. This budgeting approach is particularly valuable as it helps individuals prioritize their spending while ensuring that savings growth remains a central component of their financial plans. By establishing clear allocations, this method can assist individuals in navigating financial challenges, allowing them to maintain control over their finances even during turbulent times.

Engaging statistics reveal that a significant portion of the population struggles with budgeting and saving effectively. According to a recent survey, only about 30% of Americans have a budget in place, leading to difficulties in managing day-to-day expenses and planning for future goals. This highlights the necessity for a structured approach like the 50/30/20 rule. The simplicity of this framework not only aids in financial planning but also empowers individuals to become more mindful of their spending patterns. Adopting this rule can be a turning point for many, transforming financial behaviors and leading to increased savings and reduced financial stress.

Understanding Needs, Wants, and Savings

To effectively implement the 50/30/20 savings strategy, it is crucial to grasp the distinct categories of expenses: needs, wants, and savings. This foundational comprehension will aid individuals in accurately categorizing their financial obligations, ultimately leading to improved budget management.

Firstly, ‘needs’ refer to the essential expenses required for basic survival and daily functioning. These are non-negotiable items that individuals cannot forego without significant hardship. Common examples of needs include housing costs (rent or mortgage payments), utilities (electricity, water, gas), food, transportation (public transit or fuel), healthcare, and insurance premiums. Recognizing these fundamental expenditures is paramount, as they form the backbone of any budget.

In contrast, ‘wants’ encompass the discretionary spending that enhances one’s quality of life but is not essential for survival. These expenses, while enjoyable, can be postponed or eliminated when necessary. Examples of wants include dining out, entertainment subscriptions, vacations, and luxury goods. Understanding this distinction helps individuals recognize where they can reduce spending to allocate more towards savings or essential bills.

Lastly, ‘savings’ represent the portion of income set aside for future financial goals or emergencies. Following the 50/30/20 guideline, individuals should direct at least 20% of their income toward savings. This can take the form of contributions to retirement accounts, emergency funds, or other investment opportunities to secure financial stability. By prioritizing savings, individuals can prepare for unforeseen circumstances and build wealth over time.

Categorizing expenses correctly allows individuals to evaluate their financial landscape more effectively. This awareness not only aids in practicing the 50/30/20 rule but also fosters responsible financial habits. Distinguishing between needs, wants, and savings is therefore fundamental for achieving a balanced and sustainable financial plan.

Calculating Your 50/30/20 Allocation

The first step in the 50/30/20 savings strategy is to determine your total monthly income. This figure should include all sources of earnings, such as your salary, bonuses, side hustles, or any other income streams. If you are a salaried employee, your gross monthly income can typically be found on your pay stub; however, it is advisable to use the net income figure after taxes for a more accurate calculation of what you can spend. This approach will help provide a clearer picture of your financial landscape.

Once you have established your total monthly income, proceed to calculate the allocations based on the 50/30/20 formula. To determine the 50% allocation, multiply your net monthly income by 0.50. This portion is designated for essential expenses such as housing, utilities, transportation, insurance, and groceries. For example, if your net monthly income is $3,000, your necessities should not exceed $1,500.

The next step involves calculating the 30% allocation for discretionary spending. You can do this by multiplying your net monthly income by 0.30. This money can be spent on non-essential items such as dining out, entertainment, and hobbies. Continuing with the earlier example, 30% of $3,000 would be $900, allowing for increased flexibility in your monthly spending.

Lastly, you will determine your 20% allocation dedicated to savings and debt repayment. By multiplying your net monthly income by 0.20, you will find this figure. In our case, this would be $600 monthly, which can be directed towards your savings accounts, retirement funds, or paying off any high-interest debt. By following these steps, you can systematically apply the 50/30/20 savings strategy, enabling you to gain greater control over your finances.

The Benefits of Following the 50/30/20 Strategy

The 50/30/20 savings strategy is a budgeting framework that offers several notable advantages, making it a viable option for individuals at various income levels. One of the primary benefits of adopting this method is that it encourages financial discipline. By categorizing expenses into needs (50%), wants (30%), and savings (20%), individuals gain a clearer understanding of their financial priorities. This categorization makes it easier to track spending habits, and subsequently, individuals can make informed decisions about where to cut back if necessary.

Furthermore, the 50/30/20 strategy promotes better spending habits. By allocating a specific percentage of income to discretionary spending, individuals are less likely to splurge on impulsive purchases. For example, someone may find that by adhering to the 30% limit for wants, they can prioritize spending on experiences or items that genuinely bring happiness rather than accumulating unnecessary possessions. This method encourages mindfulness in spending, allowing individuals to derive maximum satisfaction from their expenditures.

Additionally, fostering growth in savings is another significant advantage of the 50/30/20 strategy. By allocating 20% of income toward savings, individuals can build an emergency fund or save for long-term goals such as retirement or a home purchase. This proactive approach to savings empowers individuals to establish financial security and resilience against unforeseen circumstances. Numerous success stories illustrate how people have transformed their financial situations through the consistent application of the 50/30/20 method. Many individuals report improved mental well-being, reduced financial stress, and a sustainable plan for achieving their goals as a result of this budgeting strategy.

Incorporating the 50/30/20 strategy into one’s financial routine can lead to enhanced control over personal finances, empowering individuals to secure their financial future.

Overcoming Challenges with the 50/30/20 Rule

Implementing the 50/30/20 savings strategy can present various challenges, particularly when individuals face fluctuating incomes, unexpected expenses, or difficulties in categorizing their expenses. Recognizing these potential roadblocks is vital for maintaining adherence to the rule and achieving long-term financial stability.

One significant challenge arises from income variability. Many individuals, particularly freelancers or those in commission-based roles, may struggle to allocate fixed percentages of their income during slow months. To manage this, it is advisable to establish a baseline monthly budget based on average income over several months. This method allows for a more sustainable allocation of funds while accounting for fluctuations. Additionally, consider setting aside a portion of income during higher-earning months to create a cushion for leaner periods, thereby mitigating the impact of income variability on monthly expenditure categories.

Unexpected expenses can also derail adherence to the 50/30/20 rule. Emergencies such as medical bills or home repairs can easily disrupt even the best-laid plans. One solution is to maintain an emergency fund, ideally covering three to six months’ worth of expenses. This financial buffer ensures that unforeseen costs do not force individuals to excessively dip into their discretionary spending or savings categories. Moreover, regularly reviewing and adjusting the budget to account for upcoming known expenses — such as property taxes or seasonal bills — can help individuals remain within their spending targets.

Finally, the categorization of expenses may pose a challenge, particularly when distinguishing between needs and wants. To address this, individuals can utilize financial management tools or apps that aid in tracking spending habits. By regularly reviewing these records, individuals can gain a clearer understanding of their financial behaviors and make more informed decisions to properly allocate funds in accordance with the 50/30/20 rule. This proactive approach empowers individuals to maintain control over their finances, regardless of the challenges they may encounter.

Adapting the 50/30/20 Rule to Different Income Levels

The 50/30/20 savings strategy serves as a flexible framework that can be tailored to accommodate various income levels, from low to high earners. This adaptability is crucial to making the concept accessible to a broader audience, allowing individuals to instill effective financial habits regardless of their earnings. Understanding this rule’s application helps ensure that everyone can manage their finances efficiently while preparing for future goals.

For low earners, adhering strictly to the 50/30/20 rule may appear challenging due to limited disposable income. However, the rule can be adjusted to reflect a more feasible allocation of funds. For instance, an individual earning a modest wage might consider a breakdown of 60% for needs, 30% for wants, and 10% for savings. This modification allows for the most critical expenses to be met first while still contributing to savings in a manageable way, ensuring financial stability without overwhelming pressure.

Conversely, individuals in higher income brackets have more latitude in adhering to the original structure. A high earner might allocate their budget more aggressively, earmarking 50% for needs, 20% for wants, and a substantial 30% for savings and investments. This arrangement can facilitate wealth accumulation and prepare for significant future expenditures, such as retirement or property investments. The increased savings rate can lead to achieving financial goals more swiftly and effectively.

Further, the 50/30/20 strategy remains fully adaptable for those in varying financial circumstances, such as freelancers or commission-based workers, who may experience fluctuating income. Creating a baseline average income allows for effective planning within the framework, enabling them to save during high-earnings periods and allocate wisely during leaner months.

Ultimately, the 50/30/20 savings strategy can be customized, promoting inclusivity in financial management, ensuring that individuals at all income levels can benefit from its principles effectively.

Tracking Your Progress and Adjusting Your Budget

Effectively managing finances through the 50/30/20 savings strategy necessitates constant monitoring and adjustments to ensure alignment with changing income and expenses. As such, it is imperative to regularly review your budget and financial goals. This process not only helps in tracking your savings but also fosters a proactive approach to managing your financial life.

To facilitate this, various tools are available, including budgeting apps and spreadsheets. Budgeting apps like Mint, YNAB (You Need A Budget), and EveryDollar allow users to input their income and expenses, categorize them according to the 50/30/20 guidelines, and visualize their spending habits. These applications often provide alerts and reminders which can significantly aid in maintaining financial discipline. Furthermore, they can track your progress over time, making it easier to see how well you are adhering to your budget and where adjustments might be necessary.

For those who prefer a more traditional method, spreadsheets serve as an effective budgeting tool. Creating a simple spreadsheet can help users visualize their financial standings at a glance. By manually entering income and expense data, it becomes easy to compute the percentages based on the prescribed strategy. Additionally, using spreadsheet templates allows for customization, making them flexible and adaptive to personal preferences.

It’s also essential to recognize that life events, such as job changes, family additions, or unexpected expenses, necessitate dynamic adjustments to your budgeting strategy. Revisiting and recalibrating your budget can help accommodate these changes, ensuring that your financial strategy remains relevant and effective. Regular assessments not only enhance accountability but also reinforce commitment to achieving financial goals. By maintaining an adaptable budget, you are better positioned to navigate life’s unpredictability while still working towards your savings objectives.

Real-Life Examples and Case Studies

The 50/30/20 savings strategy, which allocates 50% of income to needs, 30% to wants, and 20% to savings, has been adopted by many individuals across various income levels. One notable example is Sarah, a young professional earning $60,000 per year. By following this budgeting method, she managed to prioritize her essential expenses, such as rent and utilities, within the 50% allocation. With her needs adequately covered, Sarah allocated 30% for leisure activities and dining, while diligently funneling 20% into her retirement savings. Over three years, she watched her retirement fund grow significantly, enabling her to feel secure about her financial future.

Another success story involves the Robinson family, whose combined income is $120,000. They embraced the 50/30/20 strategy to navigate the challenges of raising two children. The family allocated 50% of their budget to necessary expenses, including mortgage payments and schooling. The 30% discretionary budget was set aside for family outings and vacations, ensuring they could enjoy life while also staying responsible with finances. The remaining 20% was directed towards a robust emergency fund, which came in handy when unexpected medical expenses arose. This structured approach not only provided peace of mind but also promoted a healthy financial lifestyle.

Lastly, consider Mike, a freelance graphic designer. As someone with an unpredictable income, Mike utilized the 50/30/20 strategy on a monthly basis by averaging his income over the previous months. During profitable months, he allocated fun money for experiences and hobbies, while in leaner months, he ensured that his essential expenditures were kept minimal. This adaptability helped him to manage his finances effectively, achieve savings goals, and maintain a comfortable lifestyle. The effectiveness of the 50/30/20 strategy across these diverse scenarios highlights its flexibility and applicability for individuals and families at different economic levels.

Conclusion and Call to Action

In summary, the 50/30/20 savings strategy offers a straightforward yet effective framework for managing finances, regardless of income level. This budgeting approach divides your after-tax income into three essential categories: 50% for needs, 30% for wants, and 20% for savings. By utilizing this method, individuals can easily establish a balanced financial plan that not only accommodates essential expenses but also allows for discretionary spending and saving for the future. The simplicity of the 50/30/20 rule makes it accessible to anyone, ensuring that it can be adapted to varying income situations and personal priorities.

Throughout the article, we have emphasized the importance of understanding one’s financial landscape before implementing this strategy. By clearly identifying needs versus wants, individuals can make informed choices that align with their own financial goals. Additionally, the allocation of a dedicated percentage towards savings creates a sustainable habit that encourages long-term financial well-being. Whether you are aiming to pay off debts, build an emergency fund, or save for retirement, the 50/30/20 strategy provides a solid foundation to achieve these objectives.

As you contemplate your financial future, we encourage you to take actionable steps towards implementing the 50/30/20 savings strategy in your own life. Begin by reviewing your current budget, categorizing your expenses, and adjusting your spending habits where necessary. Recognize the potential benefits of cultivating a mindful approach to your finances, and allow the 50/30/20 rule to guide your economic decisions. Furthermore, we invite you to explore related blog posts that delve deeper into personal finance practices, investment strategies, and tips for building wealth. The journey towards mastering your finances begins with a single step, and there is no better time than now to take charge of your future.