Making sense of personal finance often feels overwhelming, especially when you’re juggling short-term goals like paying off debt and covering daily expenses. However, one concept can dramatically change your financial outlook for the better, and that is compound interest. By understanding compound interest and starting to invest early, you can build long-term wealth and even set yourself on the path to financial independence. In this comprehensive guide, we’ll explore what compound interest is, why starting early matters, and how you can incorporate beginner investing tips to maximize your returns.

1. What Is Compound Interest?

At its core, compound interest is the process whereby your investment returns generate their own returns. In other words, you earn interest not only on the principal (the amount you initially invested) but also on the interest you’ve already accumulated. Over time, this compounding effect can grow your investments exponentially, rather than linearly.

- Example: If you invest $1,000 at a 10% annual return, you’ll have $1,100 by the end of the first year. In the second year, you earn 10% on the entire $1,100—yielding $110 in interest—bringing your total to $1,210. By the end of Year 2, that’s an extra $10 in growth beyond the simple 10% you originally calculated.

Why It Matters:

Compound interest can transform even modest monthly contributions into a substantial nest egg over the long haul. It rewards consistency and patience, making it a powerful tool in your journey toward financial independence and long-term wealth.

2. Why Early Investing Matters

The earlier you begin investing, the more time your money has to compound. Time truly is your secret weapon in growing your wealth. Even small amounts invested consistently can yield significant results when allowed to grow for decades. Conversely, the later you start, the less time you have to capitalize on the compounding effect.

The Opportunity Cost of Waiting

- Case Study: Suppose you start investing $200 per month at age 25 in a portfolio that averages a 7% annual return. By the time you’re 65, you could have over $525,000. If you wait until age 35 to start, your total drops to around $244,000—even if you keep the same investment schedule and rate of return. Waiting just 10 years can more than halve your final balance due to the lost opportunity of compounding returns.

- Inflation: Inflation gradually reduces the purchasing power of your money. By investing, you’re not only growing your funds but also fighting inflation in the long run.

3. How Compound Interest Works (Real-Life Examples)

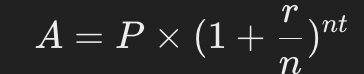

Understanding the mathematics behind compound interest can be motivating and help you see why early investing is so crucial. Let’s explore a simple formula for compound interest:

Where:

- A = the amount of money accumulated after n years, including interest.

- P = the principal investment (initial amount of money).

- r = annual interest rate (in decimal form).

- n = the number of times that interest is compounded per year.

- t = the time the money is invested for (in years).

Let’s break down a scenario:

- Principal P: $5,000

- Annual interest rate r: 8% (0.08)

- Compounding frequency n: 1 (annually)

- Time t: 20 years

Plugging the numbers into the formula:

Your initial $5,000 grows to approximately $23,300 after 20 years—an impressive return, and even more so if you continue to add to your investment each year. The difference between saving your money in a non-interest-bearing account versus investing it at even a moderate return can be staggering when compounded over multiple decades.

4. Strategies to Maximize Compound Interest

4.1 Pay Yourself First

Paying yourself first means treating your investments like a bill you must pay—before you handle other expenses. This method:

- Ensures that you consistently contribute to your investment accounts.

- Helps you avoid the temptation to skip or reduce contributions when other financial obligations arise.

Actionable Tip: Automate a transfer from your checking to your investment account on the same day you get paid. Even if it’s just $50 or $100 initially, paying yourself first ensures consistent investing.

4.2 Automate Your Investments

Modern technology and financial services allow you to set up automatic contributions to your brokerage account, retirement fund, or other investments. By automating:

- You remove the guesswork and emotional biases from your investing decisions.

- You ensure consistency, which is vital for compounding to work its magic.

- You can focus on other aspects of your personal finance, like budgeting or debt repayment.

4.3 Reinvest Your Earnings

Whether you invest in stocks, bonds, or mutual funds, one of the most significant drivers of compound growth is reinvesting dividends or interest payments. Rather than withdrawing your earnings, opt for reinvestment plans whenever possible.

- Dividend Reinvestment Plans (DRIPs): Many companies offer DRIPs that automatically use your dividends to buy more shares of the stock, amplifying the compounding effect over time.

4.4 Choose the Right Investment Accounts

Selecting the appropriate investment accounts and instruments can make a big difference in your overall returns, especially when considering the impact of taxes.

- Retirement Accounts (e.g., 401(k), IRA): In many countries, these accounts offer tax advantages—like tax-deferred growth or tax-free withdrawals—that can turbocharge your compound interest gains.

- Brokerage Accounts: Ideal for short- to medium-term goals or general investing. While they don’t offer the same tax advantages as retirement accounts, they provide more flexibility in terms of withdrawals.

5. Overcoming Barriers to Investing Early

It’s easy to understand the benefits of early investing logically. Yet many people hesitate due to fear, uncertainty, or misunderstanding. Here’s how to get past these barriers:

- Lack of Knowledge: Familiarize yourself with basic concepts like stocks, bonds, mutual funds, exchange-traded funds (ETFs), and market trends. Free resources, podcasts, and reputable finance blogs (like Wise Wallet Tips) provide excellent starting points.

- Fear of Losing Money: All investments carry risk, but you can mitigate that risk by diversifying your portfolio and focusing on long-term growth rather than short-term gains.

- Limited Funds: Even small amounts can build up over time. Robo-advisors and micro-investing apps allow you to start investing with as little as $5.

- Analysis Paralysis: With so many options—mutual funds, ETFs, stocks, bonds—it’s easy to get stuck. Start with something simple, like a diversified index fund, and learn as you go.

6. Advanced Tips for Reaping the Benefits of Compound Interest

Once you’ve established a consistent investment habit, you can explore more advanced strategies:

6.1 Dollar-Cost Averaging (DCA)

Dollar-cost averaging involves investing a fixed amount of money at regular intervals, regardless of the market’s performance. Over time, you buy more shares when prices are low and fewer shares when prices are high, which can help smooth out market volatility.

6.2 Asset Allocation and Rebalancing

- Asset Allocation: Spread your investments across different asset classes like stocks, bonds, and real estate. This diversification can protect you from market swings in any single sector.

- Rebalancing: Over time, some assets may outperform others, skewing your initial allocation. Rebalancing involves selling a portion of the assets that have grown disproportionately and reinvesting in those that have lagged, maintaining your desired asset mix.

6.3 Tax-Efficient Investing

- Tax-Loss Harvesting: Selling underperforming stocks or funds at a loss to offset capital gains can help reduce your annual tax bill, enabling you to keep more of your investment returns.

- Use of Tax-Advantaged Accounts: Max out contributions to 401(k)s, IRAs, or equivalent country-specific retirement plans. The immediate tax break or future tax savings amplify the benefits of compound interest.

6.4 Leveraging Employer Matching

If you’re employed and have a company-sponsored retirement plan (like a 401(k) in the U.S.), your employer may match a portion of your contributions. This matching is essentially free money added to your investments, further accelerating the compounding effect. Always contribute at least enough to get the full match if it’s offered.

7. Conclusion and Key Takeaways

Compound interest is a financial phenomenon that rewards consistent, long-term investing. Starting your investment journey early—no matter how small your initial contributions—maximizes the time you have for compounding returns. By paying yourself first, automating your investments, and reinvesting your gains, you set the stage for steady, exponential growth. Overcoming barriers such as fear, lack of knowledge, and limited funds is easier when you break down the process into manageable steps and focus on building wealth methodically.

Remember: You don’t need a finance degree or huge sums of money to benefit from compound interest. Patience, consistency, and the courage to start early are the real game-changers. Commit now to contributing even a modest amount, and watch your money work for you over time.

- Start Today: If you haven’t begun investing, open an account at a reputable brokerage or robo-advisor. Automate a small monthly deposit, and gradually increase the amount as your budget allows.

- Review Your Portfolio: If you’re already investing, take time to evaluate your asset allocation and see if you can optimize for maximum compounding.

- Stay Informed: Follow trusted sources, listen to finance podcasts, and keep learning. Knowledge is your best hedge against fear and uncertainty in the markets.

By exploring these posts, you’ll continue to expand your understanding of how to manage your money wisely, make informed financial decisions, and stay on track toward long-term wealth and financial independence.

Compound interest isn’t just a neat math trick; it’s a powerful mechanism for creating and preserving wealth. The key is to start as soon as possible. No matter how small your initial contributions, begin now and allow compound interest to work its magic for you. Your future self will thank you.